5 Year Cds Spread Definition

Cds Spreads As A Measure Of Risk Le Blog De Ufm Team

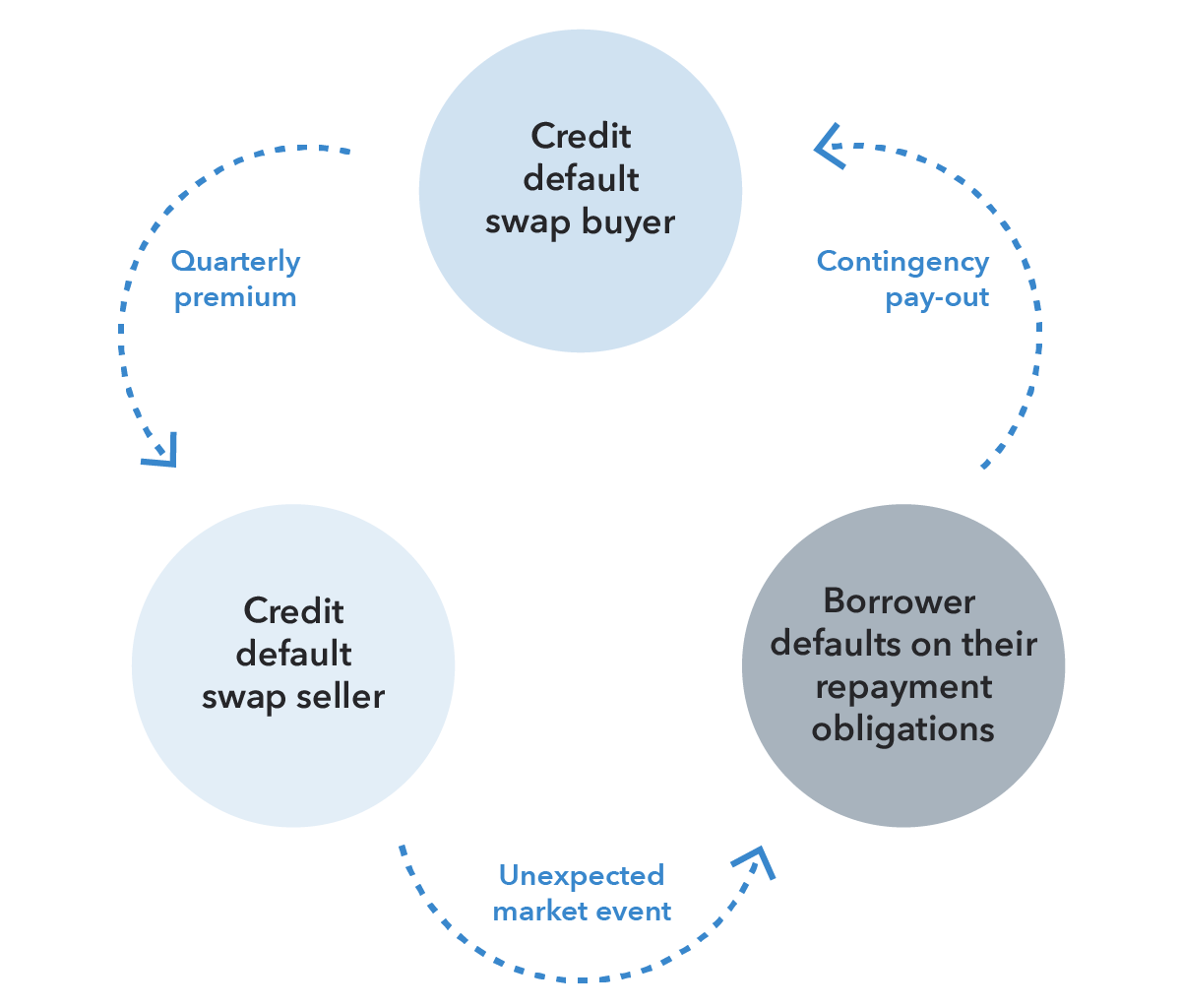

Credit Default Swaps Cds

Sovereign Cds Q A Bond Vigilantes

:max_bytes(150000):strip_icc()/CorporateBonds_CreditRisk22-8c12f1dbc1494f28b3629d456fb4fa63.png)

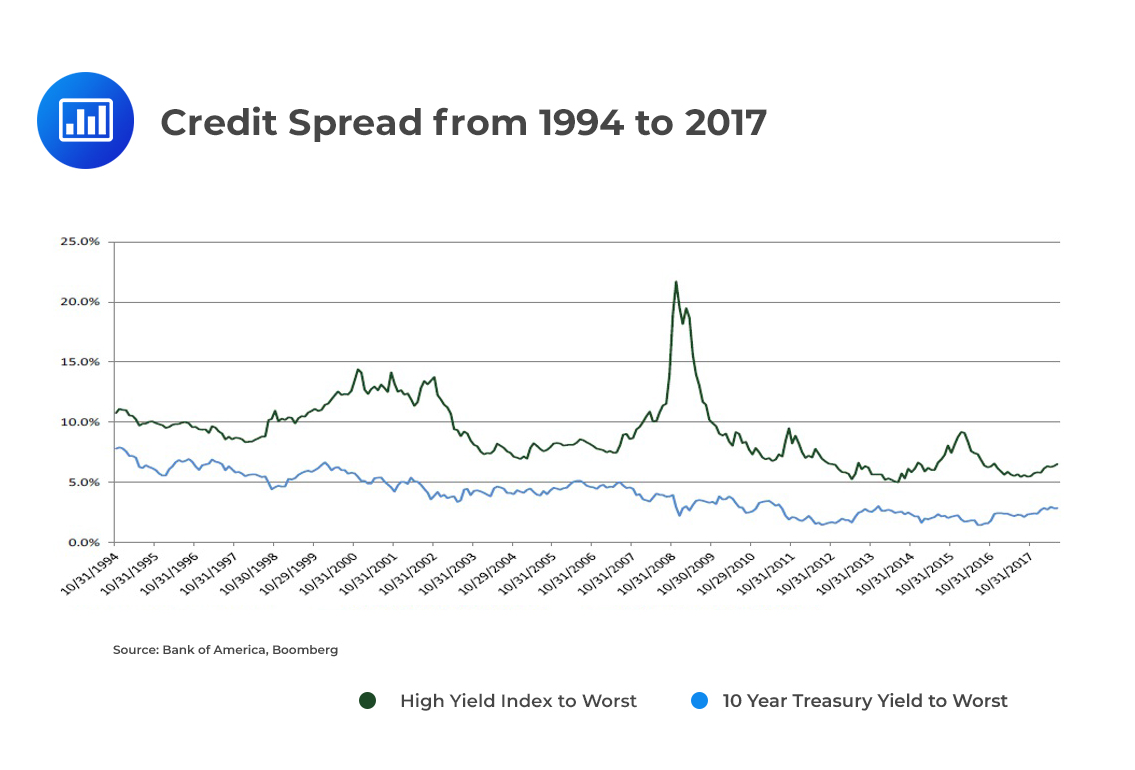

Corporate Bonds An Introduction To Credit Risk

What Is A Credit Default Swap Cds Meaning And How They Work Ig Uk

Understanding Credit Default Swaps Pimco

This page provides vietnam credit default swap historical data vietnam cds spread chart vietnam cds spread investing and data.

5 year cds spread definition.

Spread Risk And Default Intensity Models Frm Part 2 Analystprep

How To Read Cds Prices Featuring Portugal Ft Alphaville

:max_bytes(150000):strip_icc()/dotdash_Final_Introduction_To_Counterparty_Risk_Feb_2020-02-5477c45c30ee48b4b09617f3b88300f4.jpg)

Introduction To Counterparty Risk

Sovereign Credit Risk And Exchange Rates Evidence From Cds Quanto Spreads Sciencedirect

:max_bytes(150000):strip_icc()/dotdash_Final_Line_of_Credit_LOC_May_2020-01-b6dd7853664d4c03bde6b16adc22f806.jpg)

Line Of Credit Loc Definition

A Security Guard Protects An Eleven Year Old Girl Who Is Being Targeted By A Gang For Participating As A T Data Science Infographic Data Science Data Scientist

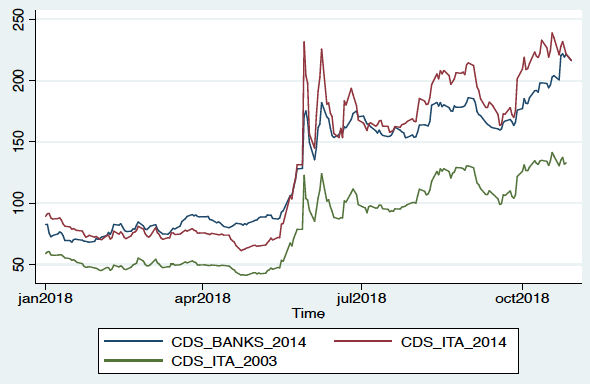

Sovereign Debt Banks And Firms Investment In Italy Vox Cepr Policy Portal

Measuring Sovereign Risk Are Cds Spreads Better Than Sovereign Credit Ratings Rodriguez 2019 Financial Management Wiley Online Library

Skye Mastercard Allows You To Convert Purchases Of 250 Or More To Your Choice O Credit Ca With Images Credit Card Online Credit Card Website Credit Card First

Http People Stern Nyu Edu Adamodar Pdfiles Cfovhds Riskfree Spread Pdf

Cis And Trnas Isomerism Of Alkenes In Naming Iupac Nomenclature Chemistry Basics Organic Chemistry Study Chemistry

Credit Default Swaps Part I Of Iii A Brief History Of Mechanics Product Types And Standardization Seeking Alpha

Https Www Imf Org Media Files Publications Wp 2019 Wpiea2019292 Print Pdf Ashx

/DurationandConvexitytoMeasureBondRisk2-0429456c85984ad3b220cd23a760cda5.png)

Duration And Convexity To Measure Bond Risk

Https Www Econstor Eu Bitstream 10419 206543 1 1680836471 Pdf

A Guide To The Five Lands Of Italy Quranmualim Learn Islam Learning Drives Learn Islam Learn Quran Listen To Quran

If You Re On Your Community Association S Board You Should Be Familiar With Your Code Of Ethics Excellent Example To Get Your Bo Code Of Ethics Coding Ethics

How Should We Be Thinking About Credit Spreads Seeking Alpha

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gct5umyzanrpm0rhbywgikdlydmfwfmg3i4zx220sxs 8fgmbtg7 Usqp Cau

Napkin Finance Put Option Option Trading Finance

Https Www Moodysanalytics Com Media Article 2016 Cds Implied Edf Measures Fair Value Cds Spreads At A Glance Pdf

:max_bytes(150000):strip_icc()/pen-money-office-business-product-cash-859216-pxhere.com-e976a1beceae444d821a0ea653ec4dc8.jpg)

Credit Default Swap Cds Definition

How U S Structured Finance Has Changed Since The Credit Crisis S P Global Ratings

The Generation Between Gen X And Gen Y Call Us The Xennials Generation Generations Quotes Generational Differences

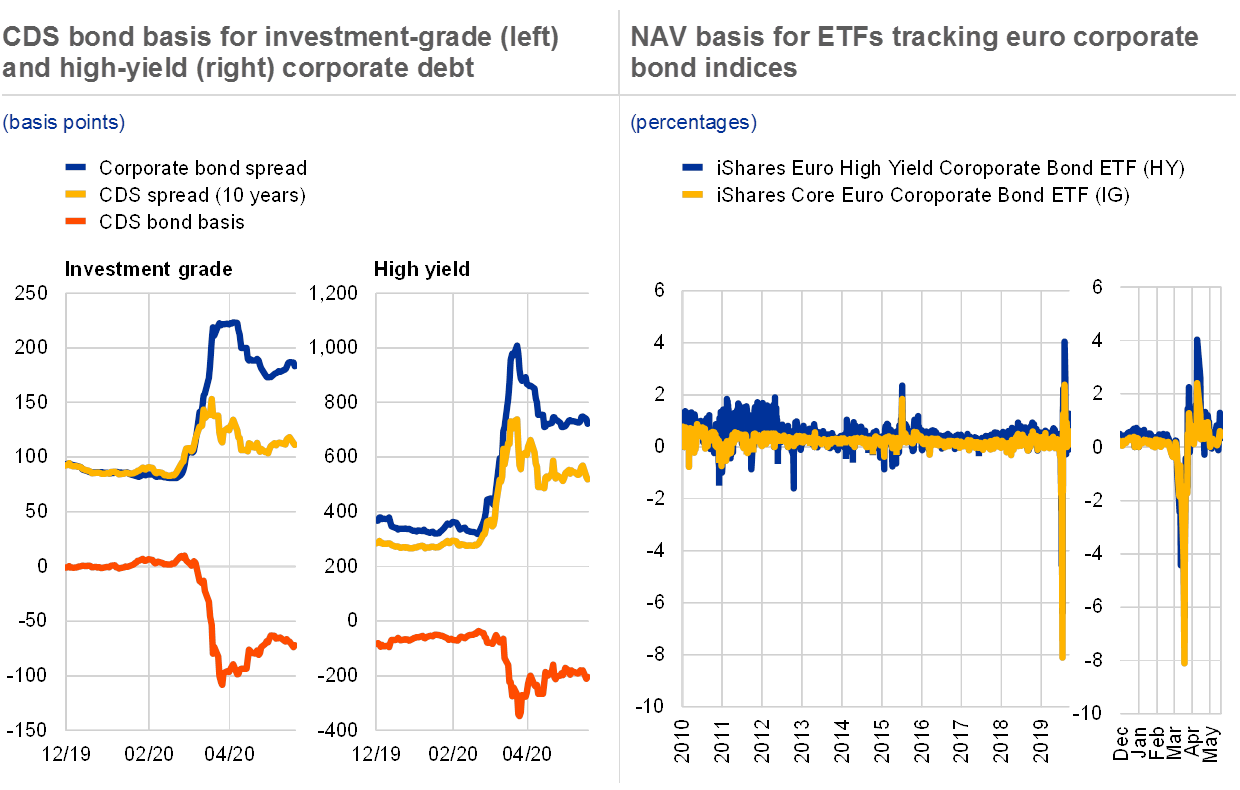

Financial Stability Review May 2020

Credit Default Swaps Cds Intro Video Khan Academy

/Convexity22-0370dbde8e1c4a958bff8b670bf8bf5c.png)

Convexity Definition

Fantasy Faire Magic Music Festival Jefferson Airplane The Doors Grassroots Iron Butterfly Cou Music Festival Poster Music Concert Posters Concert Posters

Are Singapore Bank Bonds Close To Risk Free Bondsupermart

Do Your Little Dinosaurs Have A Case Of The Wiggles Have Them Stand And Follow Preschool Songs Dinosaurs Preschool School Songs

Definition And Examples Of Narratio In Classical Rhetoric Rhetoric Definitions Example

Https Www Moodysanalytics Com Media Article 2020 Weekly Market Outlook Coronavirus May Be Black Swan Like No Other Pdf

Midi Hits Backing Music For Musicians Singers Faqs Midi In 2020 With Images Music Download Karaoke Cds Free Mp3 Music Download

Sermabeikian Patricia March 1994 Our Clients Ourselves The Spiritu Social Work Practice Social Work Spirituality

:max_bytes(150000):strip_icc()/Best6-monthCDs-89eb38cbf5094cd4aab4b4559d76c083.jpg)

Certificate Of Deposit Cd Definition How Cds Work

Mental Fitness Challenge Boxed Set Bullet Journal Workout Bullet Journal 30 Day Challenges Bullet Journal 30 Days

Drsk Bloomberg Deafult Risk

Unofficial Designs Joseph Novak Pastor Designer Church Music Liturgy Songs

Https Helda Helsinki Fi Dhanken Bitstream Handle 10227 222479 Quang Pdf Sequence 1 Isallowed Y

Dad Personalized Pocket Pillow Father S Day Gifts Gifts Etsy In 2020 Unique Gifts For Dad Christmas Presents For Dad Funny Gifts For Dad

Table Of Content 1 Introduction Of Business Essentials Business Ethics 2 Business Ethics Business Essentials Ethics Meaning

Sewing Room Clock 11 Craft Room Wall Decor Quilting Etsy In 2020 Button Crafts Crafter Gift Craft Room Decor

Golf Party Invitations Template Blue Green Birthday Invitations Printable Templates Golf Invitation Party Invite Template

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcsyvliobz84dts7rfsx46mbncvhnvpijti0tdbyc75qfufvunxm Usqp Cau

Source : pinterest.com